As always, this lesson is not intended to be professional advice. This is simply lesson material for ESL students in a Managerial Economics and International Finance class. Posted here for their use or for helping other students.

There are 3 main Financial Documents you should be familiar with. Each paper is typically published once a year, so we say they are annual reports (年波).

**Please notice that all three documents only count and discuss EXPLICIT COSTS (明确的成本). These documents are working with numbers and math, so the Explicit Costs includes only the money paid out to market-suppliers. It does not include any of the Implicit Costs like time and effort that the owner loses. Therefore, the profits we see are only ACCOUNTING PROFITS (会计利润). You can find a more detailed explanation of Costs and Profits here.

The Income Statement (损益表)~ Tells the reader very specifically (with a lot of detail):

- How much REVENUE (收入) they earned and where it came from,

- Revenue = Income, Sales, Yield, Gains

- How much COST (成本) they had and what the money was spent on,

- Cost = Expenses, Loss

- How much PROFIT (收益) was left at the end and what of that the owners will be paid.

- Profit = Returns, Sales, Yield, Income

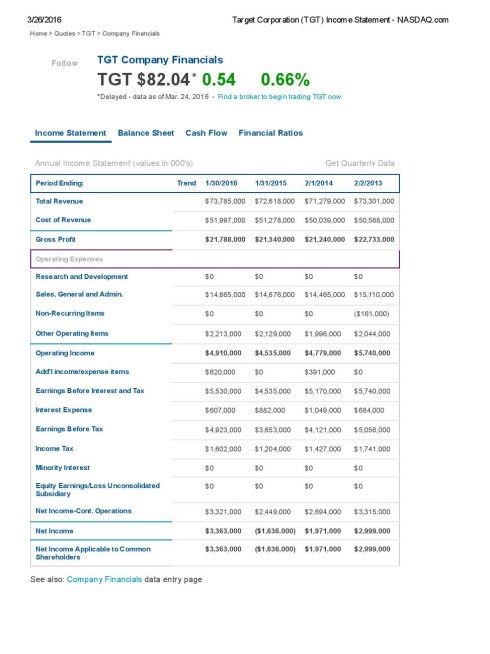

EXAMPLE OF AN INCOME STATEMENT:

STEP 1: COST OF PRODUCTION

- Total Revenue (收入) = The final revenue or income the company made from doing normal business (selling products, offering services, renting its building, etc.)

- Cost of Revenue (直接成本) (also called direct costs or COGS) = Total cost of creating and delivering your product to the customer. Raw materials, inventories, tools, labor, shipping, etc.

- *This only includes the costs related to the products themselves — not administrative, legal, etc.

- Gross Profit (毛收入) = TOTAL REVENUE – COST OF REVENUE

- Tells us how much revenue remains after the products are paid for.

- Helpful if you want to compare competitors – Is Xiaomi or Huawei making a better profit on their phones?

- Helpful if you want to test which product will make you the better profits.

- **You should be familiar with Profits (收益). But GROSS PROFIT is NOT the money the owners take home. Gross Profit is NOT Profit = Revenue – Cost. Gross Profit is a specific kind of profit (Revenue – Cost of Products). When you hear people in English talk about Profits, they normally mean NET INCOME, which comes at the end of this article!

STEP 2: OPERATION EXPENSES (经营费用)

- This includes all those random other costs you need to pay for in addition to the product costs.

- Research & Development (研发) = All costs associated with research and development (new products, new tools, new methods or systems)

- Sales, General, Administration – Also called SGA

- Sales (销售) = all the costs that went into actually selling the product (rent for the stores, advertising, taxes, marketing, wages for the sellers, etc.)

- General (一般费用) = All the normal costs for running the business itself. Taxes, Insurance, Wages for the Departments like Finance, Auditors costs, Office Supplies, Business Training, Business Trips, etc.

- Administration (管理成本) = The salaries for your executive staff (CEO, CFO, etc), all those costs required for doing the paperwork of your company — registration, licenses, etc.

- Non-Recurring Costs (非循环)

- Most of the Operating Expenses above will be repeated year after year. Maybe the cost will change with inflation (通胀) or deflation (通货紧缩), but it will still show up every year.

- Non-Recurring Costs don’t do that — they only happen once.

- For example, you sold a building this year. You probably won’t do that again normally, this year was just special.

- Other Operating Income

- Anything that didn’t fit above.

STEP 3: Remaining Costs

- First total everything from before:

- Total Revenue – Cost of Production = Gross Profit.

- Gross Profit – Operating Expenses = Operating Income (营业收入)

- Additional Income / Expense Items = Any random money you earned or spent that didn’t fit into the categories listed above. (For example, interest you earn on your loans or costs, money spent renting a lawnmower, income from letting other people use your company logo in a movie, etc.)

- Income = Revenue | Expense = Costs

- Earnings Before Interest & Taxes (EBIT) (利息和税前利润)

- Operating Income – Additional Income / Expense Items = EBIT

- How much Revenue now remains before you pay off your loans or taxes.

- Interest (利息费用)

- All the money you pay towards debts you have because you borrowed money from someone (for example, interest on loans, etc.)

- Earnings Before Taxes (EBT) (税前收入)

- EBIT – Interest = EBT

- Taxes (税收)

STEP 4 – NET INCOME

- Net Income – Continued Operations

- This line tells you all the EARNINGS (revenue) left that the business keeps. But it DOES NOT include one-time events or costs from ending operations (shut down costs).

- Net Income from Cont. Operations = Net Income – Discont. Operations

- Net Income (净收入)

- Net Income = EBT – Taxes +/- Discontinued Operations

- Usually Net Income = EBT – Taxes

- But Sometimes you’ll find companies also add or subtract any other relevant costs / income that didn’t fit in the above categories such as costs / income from ending some operations (shutting down a factory)

- This is the final number – this is what we usually mean when we talk about PROFITS. This is the money the owners could take home if they wanted!

STEP 5 – OTHER INFORMATION INCLUDED

- Minority Interest (少数股东权益)

- Also called NCI or Non-Controlling Interest

- How much of the company’s equity / income does not belong to the majority shareholders (大股东). A majority shareholder (usually the parent company) owns between 50%-99.9% of the company. The minority shareholder owns less than 50%. On the income statement, the corporation will say how much of the equity should belong to the minority shareholders under minority interest.

- Equity Earnings / Loss of Unconsolidated Subsidiaries

- This occurs when one company invests in or owns other companies. For example, Google often invests in smaller companies beneath them. These are the earnings or losses associated with these ‘investments.’ We mostly include them to show readers how much we are earning or have put at risk through our investments.

Leave a comment