**As always, my work is designed with Chinese ESL student in mind. Please consider this when reading.

Corporate Finance has 3 main types of Financial Documents:

- Balance Sheet ~ Value of the Company (How it is divided between Debt and Equity)

- Income Statement ~ Specific Use of Assets and Liabilities

- Cash Flow Statement ~ How Cash is Handled from the moment it enters the company until it leaves.

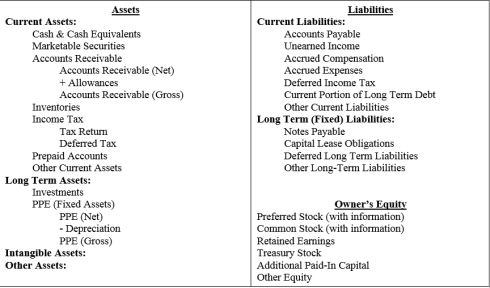

Balance Sheet

We all know that Revenue has to be bigger than Costs/Expenses if the company is going to be successful (Revenue – Cost = Profit). And if you are a financial manager, your legal responsibility is to increase profits for the Shareholders (earn a profit).

However, for years all that companies worked with were Income Statements. Unfortunately many of them quickly realized they could hide money away in methods not put on the Income Statement. Not only that, but the Income Statement didn’t really outline all of the important factors used in looking at Profit. So now we have the Balance Sheet -a financial document intended to make everything more honest and clear.

The Balance Sheet summarizes the Assets, Liabilities, and Equity at a certain date.

- It is an overall summary of what the company looks like.

- It explains to the Business how well the company is functioning

- It explains to Owners how well their Equity is doing

- In general, it tells us if the company will be profitable or not.

For example, how much is the company worth July 2016?

General Equation (Assets = Equity – Liabilities)

- Assets = Everything owned by the company. Obtained by either creating capital or obtaining debts (borrowing money)

- Current Assets –Assets that will be turned into cash within 1 Year

- Long-Term (Fixed) Assets – Assets that will be turned into cash within more than 1 Year

- Intangible Assets – Assets that you cannot see, but that still exist

- Liabilities = All the debt the company has to pay

- Current Liabilities—Debts to be paid this year.

- Long-Term Liabilities—Debts to be paid in more than 1 year.

- Equity (Net Worth) = Assets – Liabilities (The Company’s Value for the owners)

- Owner’s Equity (Owner’s Investment – Owner’s Withdrawals from the Company +/- Net Income/Loss)

- Retained Earnings

- Net Profits or Losses

The Balance Sheet will be organized according to the “Liquidity” of the category (meaning how quickly that category of assets, liabilities, or equity can be changed into cash). The farther down the list we go, the less liquid the categories become.

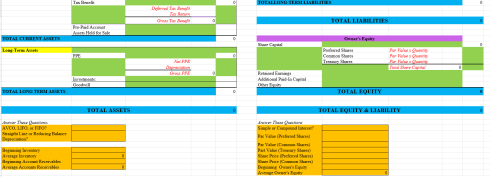

EXAMPLE

Tags: Balance Sheet, business, Consultant, Finance, Financial documents

I’ve now expanded this file to include:

I’ve now expanded this file to include: